The India beer market is becoming increasingly regional. While national demand remains resilient, growth is no longer being driven uniformly across the country. Instead, a handful of states are shaping industry performance through their influence on volumes, pricing, premiumisation and profitability.

India consumed nearly 345 million cases of beer in 2023, making it one of the fastest-growing beer markets in the Asia-Pacific region. The market is expected to maintain a CAGR of over 6% through the next decade. It is going to be driven by urbanisation, rising disposable incomes, and a young legal-drinking-age population. Yet those national growth numbers tell only part of the story.

The real action is unfolding at the state level.

For brewers, marketers and suppliers, four states are increasingly shaping the industry's direction: Telangana, Karnataka, Maharashtra and West Bengal. What makes them important is not simply their size. Each represents a different reality of India's beer business. Telangana is a volume powerhouse struggling with profitability pressures. Karnataka is testing the limits of taxation-led pricing. Maharashtra is emerging as a premiumisation hub. West Bengal remains one of the country's most stable alcohol markets.

Together, they explain where India's beer industry stands in FY26 and where it may be headed next.

Telangana: India's Biggest Beer Engine Faces a Reality Check

For years, Telangana has been one of the most important beer markets in the country. The state routinely sells between 45 lakh and 55 lakh cases of beer every month, supported by Hyderabad's large technology workforce, migrant population and strong urban drinking culture.

The numbers remain enormous.

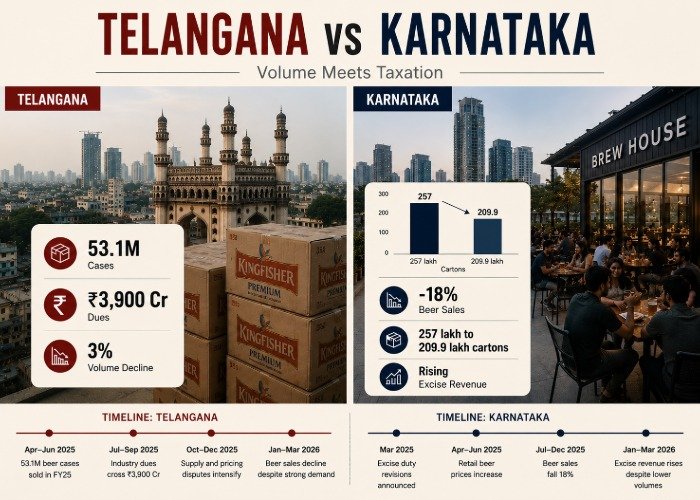

In FY24, Telangana sold 54.8 million cases of beer. In FY25, that figure fell to 53.1 million cases, marking a 3% decline. While the drop may appear modest, it exposed deeper pressures within the market. Outstanding dues owed to the liquor industry reportedly crossed ₹3,900 crore, while pricing disputes led to supply disruptions involving major brewers.

The challenge became more visible in FY26.

Beer sales reportedly fell 9% year-on-year, dropping from 536.13 lakh cases to 387.34 lakh cases, even as overall liquor revenues reached a record ₹40,209 crore. At the same time, stronger spirits began outperforming beer in several consumption periods, particularly after retail beer prices increased from around ₹150 to ₹180 for a 650 ml bottle.

For marketers, Telangana remains indispensable because of its scale. For suppliers and brewers, however, it has become a reminder that volume alone no longer guarantees profitability.

Karnataka: The State Testing India's Price Ceiling

If Telangana dominates on volume, Karnataka continues to dominate influence.

Bengaluru remains India's most mature beer city. The state helped build the country's craft beer ecosystem, accelerated premium beer adoption and created one of India's strongest on-trade markets. Many of the trends that later spread across urban India first gained traction in Karnataka.

But FY25 raised uncomfortable questions.

Beer sales in Karnataka dropped by more than 18% during the first half of 2025. Between January and June, sales fell from 257 lakh carton boxes to 209.9 lakh cartons. The steepest decline came in January, when volumes plunged 30.6%, while April and May, traditionally peak summer months for beer consumption, also recorded declines of 16% and 26% respectively.

The decline came after multiple revisions in additional excise duties and licence fees over the past two years.

What makes Karnataka particularly important is that revenues continued to rise despite lower consumption. The state's excise collections increased even as beer volumes declined, creating a situation where government earnings improved while brewer volumes weakened.

For the broader industry, Karnataka has become a real-time experiment in price sensitivity. If beer demand can soften in a market long considered India's beer capital, the implications extend well beyond the state itself.

Maharashtra: Where Premiumisation Is Becoming Business Strategy

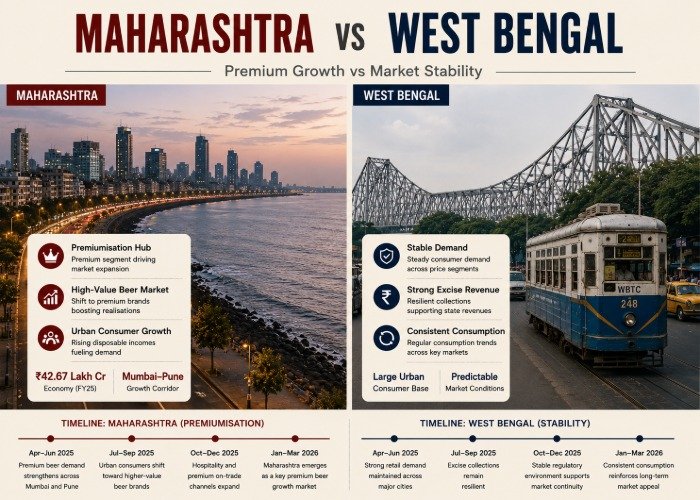

Maharashtra's beer story is less about volume and more about value.

The state's importance comes from its concentration of high-spending urban consumers across Mumbai, Pune and Nashik. Maharashtra also remains India's richest state by GSDP, with an economy valued at roughly ₹42.67 lakh crore in FY25, making it one of the most attractive consumption markets for premium alco-bev brands.

That economic strength is increasingly visible in beer.

Industry players continue to view Maharashtra as a critical market for premium and imported labels. State excise records show sustained beer sales activity across major urban centres, while brewers are increasingly using Maharashtra to test premium launches before expanding them nationally.

The trend aligns with broader shifts across India's alco-bev market, where younger consumers are showing greater willingness to spend on differentiated products rather than simply consuming higher volumes. Premium lagers, wheat beers and international brands are becoming more visible across urban retail and hospitality channels.

For suppliers, Maharashtra's significance extends beyond consumption. Premiumisation increases demand for better packaging, specialty ingredients, imported hops and value-added brewing inputs. In many ways, the state has become India's most important beer market for future value growth.

West Bengal: The Market That Keeps Delivering

West Bengal rarely generates the headlines that Karnataka or Telangana do.

Yet it remains one of India's most dependable alcohol markets.

Industry reports consistently place West Bengal among the country's leading consuming states, supported by a large urban population, a dense retail network and relatively stable demand patterns. The state recorded strong excise revenues in recent years, including record liquor sales periods that generated over ₹235 crore in revenue during key festive windows.

For brewers, the appeal of West Bengal lies in predictability.

Unlike several southern markets that have experienced pricing disputes, supply disruptions or repeated tax revisions, West Bengal has largely remained a stable operating environment. That consistency allows companies to plan distribution, inventory and long-term investments with greater confidence.

In an industry increasingly shaped by regulatory uncertainty, stability itself has become a competitive advantage.

Four States, Four Different Futures

The most interesting aspect of India beer market FY26 is that growth is no longer being driven by a single factor.

- Telangana continues to prove the power of scale, even as profitability becomes harder to protect.

- Karnataka is showing how taxation can reshape consumption behaviour in a mature beer market.

- Maharashtra is emerging as the industry's premiumisation laboratory.

- West Bengal remains a reminder that stability still matters.

For marketers, suppliers and brewers, these four states offer a clearer picture of India's beer future than any national growth forecast. The industry's next phase will not be determined by how much beer India drinks. It will be determined by where that beer is being consumed, how consumers are choosing to spend, and which states continue to create conditions for sustainable growth.